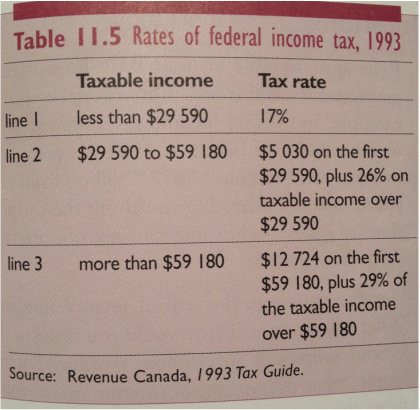

Above are the 1993 income tax rates as taken from the Made in Canada textbook.

Income tax: most important source of revenue for federal government (50% of total collected taxes), tax paid on income annually

Government Revenue: money earned primarily by taxing (includes federal income tax, excise tax, corporate income tax, unemployment insurance contributions, etc.) Direct tax: tax levied on and directly paid by a person or corporation. Direct investment can be made to establish or take over a business already in existence. Much US investment in Canada has been in the form of direct investment. Regressive tax: as income increases, the percentage paid in tax regresses or declines. Provincial sales taxes and local property taxes are examples of regressive taxes.

|

Article Excerpts:"Your RRSP can be a great vehicle to save for retirement, but you can’t keep your plan around forever. You can have an RRSP until the end of the year in which you reach age 71, but then your plan matures and you’ll need to wind up your RRSP by the end of that year. Most people convert their RRSP to a registered retirement income fund (RRIF), but that’s a story for another day.

You can gain the benefit of RRSP deductions even after the year you turn 71 if you make excess contributions to your RRSP before you wind-up your plan at the end of the year in which you reach 71. Now, you should be aware that a penalty will apply for the overcontribution, but the tax savings from the RRSP deduction will far outweigh that penalty. Consider Jack’s example. Jack turned 71 earlier this year, and so he has to wind up his RRSP by the end of December. Now, Jack has earned income this year of $134,833. This will provide Jack with RRSP contribution room next year of $24,270 ($134,833 x 18 per cent) – the maximum in RRSP contribution room possible for 2014. (Earned income in one year provides RRSP contribution room in the following year, at the rate of 18 per cent of your earned income). The problem? Although Jack will have $24,270 of RRSP contribution room in 2014, he won’t have an RRSP in 2014 since he’s required to wind up his plan by the end of 2013. Does Jack lose the ability to make a contribution for 2014 and claim an RRSP deduction in that year? No. Jack is going to make his 2014 RRSP contribution in December, 2013, prior to winding up his RRSP. Provided that Jack has already maximized his RRSP contributions for 2013, making an additional contribution of $24,270 in December will result in an overcontribution to his RRSP, and will result in a penalty of $223 for that month. Taxpayers are allowed a $2,000 overcontribution without penalty, so Jack will face a penalty on an overcontribution of $22,270 ($24,270 minus $2,000). The penalty is 1 per cent a month, so the penalty for December would be $223 ($22,270 x 1 per cent). The good news? On Jan. 1, 2014, Jack’s overcontribution problem disappears because he will be entitled to $24,270 of RRSP contribution room on that day thanks to his earned income in 2013. So, the overcontribution made by Jack will provide him with a $24,270 RRSP deduction in 2014, which will save him $11,264 in income taxes in 2014 since he’s in the highest marginal tax bracket in Ontario. Jack is glad to pay the $223 penalty to save $11,264 in taxes." |